Risk management rules within an organization can differ significantly: whether you choose to track only one general certificate of insurance per vendor or require vendors to provide different insurance proofs for each project they work on. Here we explore all the different ways you can configure BCS to fit your needs.

Configuration Steps:

These are high-level steps in your process of configuring BCS. Further below we dive into each of these in more detail.

1. Set up your locations with their respective ownership entities. Choose if you have a single location configuration or a multiple location configuration:

2. Set up your requirement categories. What are the different templates of insurance requirements - what policies, limits and endorsements are your vendors asked to provide? You might have different requirements based on the level of risk their trades represent - i.e. a dry cleaning vendor doesn't represent the same level of risk as your scaffolding contractor.

3. Location-specific

4. Determine if you need to add more than 1 job per vendor, or more than 1 lease per tenant. As a rule of thumb, ask yourself "Do I need my Vendor to give me a different COI depending on what project/location they perform work?". If the answer is 'no', then 1 vendor = 1 job. Our architecture allows you to setup any configuration that best fits your business.5. Choose the "Labels" that make most sense to your organization (do you track "tenants" or "subcontractors", "vendors" or "franchisees"?)

Understanding the BCS Architecture

About the Vendor-Job & Tenant-Lease Relation

In BCS, Vendors have the ability to provide multiple proofs of compliance, called "jobs", just like you can track more than one proof of insurance for the same Tenant by adding additional "leases". Think of these "jobs" and "leases" as subfolders, with each job being a "child" of the vendor and each lease being a "child" of the tenant. This relationship is illustrated below:

Flexibility of Requirements

There are 2 elements in a job/lease that will dictacte what the Vendor/Tenant's insurance has to include:

By combing these 2 elements in different ways, you can track virtually any compliance rules.

Locations

You'll first need to evaluate if you are a single location or multiple location organization, from a COI tracking perspective.

A) Single Location

If your company operates from a single site, you clearly fall under a single location configuration. Additionally, if you have multiple sites but the specific location where a vendor is working does not impact the requirements for the Certificate of Insurance (COI), you would still be considered a "single location" type of organization.

B) Multiple Locations

If your organization operates in real estate or construction and you need to track varying insurance requirements from your vendors based on their work location, this configuration will suit your needs. Additionally, if your organization has multiple sites and requires different Certificate of Insurance (COI) stipulations depending on the specific location, you will also fall under this configuration.

Each Location can represent:

- a project

- a hotel

- a property

- an asset

Each location within BCS is set up with its geographical address, as well as a Certificate Holder and Ownership Entities.

By setting up your Requirement Categories in a way that requires the location's owner(s) to be listed as additional insured, the app will automatically track the ownership entities as additional insured based on the location associated with the job/lease. This ensures that the appropriate parties are covered and protected.

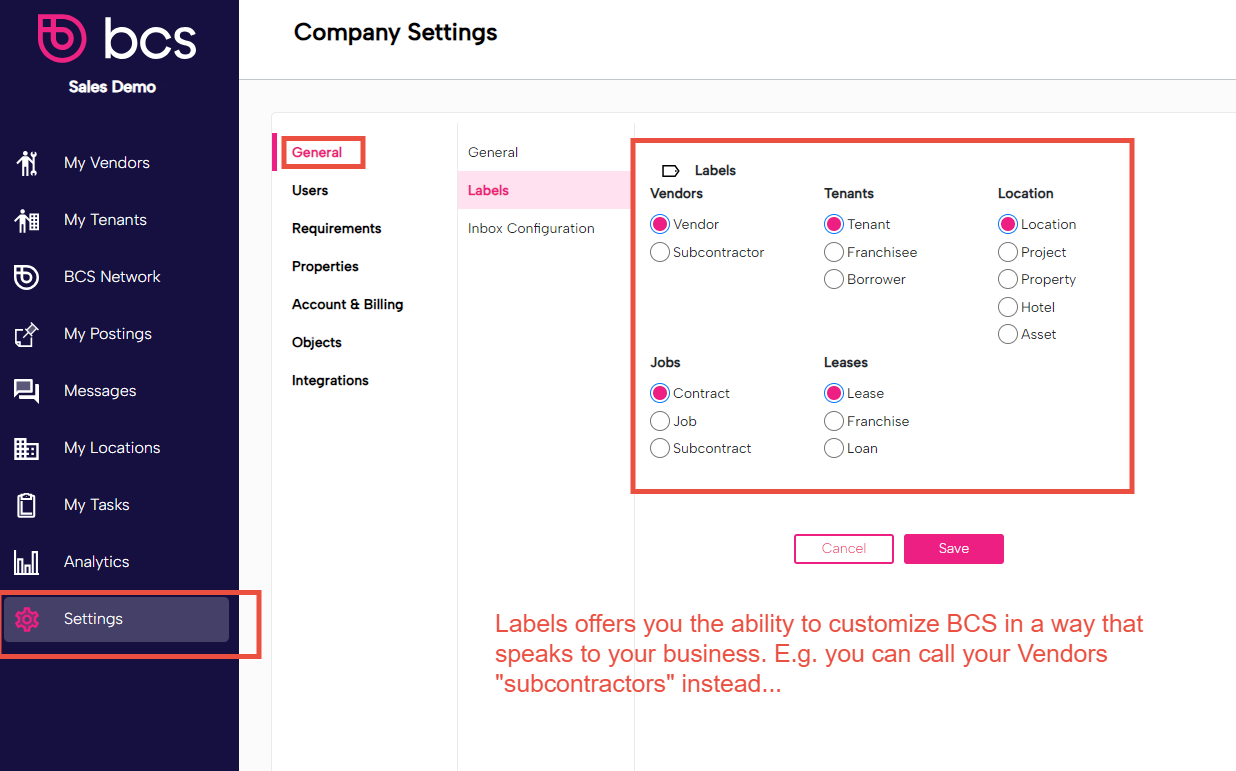

Changing Labels to fit your Business

Go to "Settings" to change the labels. Your tenants might instead be "Franchisees" or "Borrowers". Likewise, you might refer to your locations as "Projects" or "Properties" instead.